Can You File Taxes on a Postcard? Sure, if Your Tax Returns are Simple

Our society is so simple and so standardized...NOT!

This post contains affiliate links. See Disclosures for details.

In an effort to simplify the tax code, lawmakers aggressively pushed and passed the Tax Cuts and Jobs Act of 2017. One of the first claims of the Trump administration was to reform the tax code and streamline tax filings so far as to allow people to file their taxes on a postcard-sized piece of paper! Do I think it’s possible? Yes! But I think it will only be applicable for taxpayers with little to no complications in their tax returns.

The basic formula for calculating taxes remains the same. I’ll explain the different components at their simplest level in this post. I am by no means a tax expert but I do believe everyone should have a basic understanding of how their taxes are calculated. Then you can determine for yourself if in fact simplifying tax filings to a postcard is a lofty goal. To make it easier, we’ll apply the rules in effect for an individual filing their taxes for the 2018 tax year (for the tax return to be filed in 2019).

As pretty as a postcard...

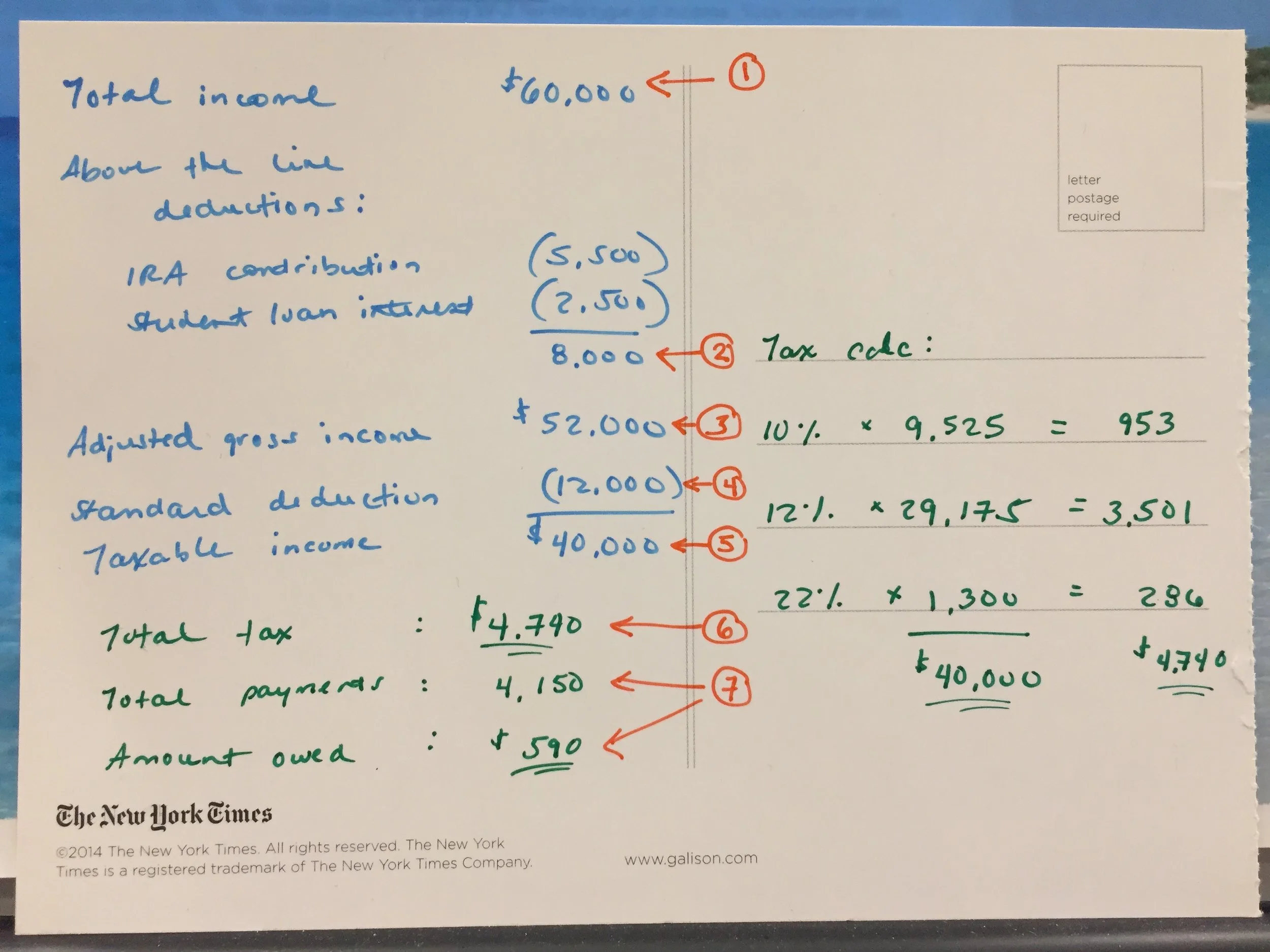

1. Total income – This is typically your salary, after any tax beneficial deductions such as 401k, medical premiums, etc. You would typically get a W-2 for this type of income. Total income also includes any interest or ordinary dividends from investments.

2. Above the line deductions – These are deductions that fall above the adjusted gross income line. These include contributions to a traditional IRA, student loan interest deductions, certain work related expenses, etc. For additional examples refer to the list here. These deductions are typically preferable to “below the line deductions (See item 4) since you don’t need to itemize them to deduct them. However, these deductions are still subject to certain rules and phase-outs. For example, see my article on the Student Loan Interest Deduction.

3. Adjusted gross income (“AGI”) – This is your total income (item 1) less your above the line deductions (2).

A detailed look into one with more deductions.

4. Below the line deductions – This is the larger of your standard deduction ($12,000) or itemized deductions. If you claim the standard deduction, it’s straightforward; you reduce your taxable income by $12,000, no support needed. If you itemize, as the name implies, you have to take into account each “item” to deduct. These items include mortgage interest, real estate taxes, state and local taxes and charitable contributions. You will need backup (support, receipts, etc.) to show you have made these payments during the year you are claiming them. Note there are limits to some of these deductions. For example, there is a limit for the combined amount of state and local income and real estate taxes you can deduct up to the amount of $10,000.

5. Taxable income – This is the amount you arrive at once you take your AGI (item 3) and subtract out your below the line deductions (item 4). This is the amount you use to calculate your total tax.

6. Total tax – This is the amount of taxes you owe for the year. Unfortunately, we do not have a flat tax rate system so we cannot simply apply 22% to the taxable income line and get the amount you owe. The US has what is know as a progressive tax system, which means, as your income grows and you meet the threshold for a higher tax bracket, you’re going to be paying more taxes for those dollars that fall within that higher tax bracket. The highest bracket you’re in is your “marginal tax rate”. Read more about determining your income and tax brackets.

7. Payments/refund/amount owed – To determine if you will get a refund or if you owe the IRS, you need to take a look at what you have paid throughout the year in payroll withholdings. If the amount withheld for federal taxes during the year is more than the total tax in item #6, then you will receive a refund. If amount is less than the total tax in item #6, then you will owe money to the IRS. Note, your withholdings are determined based on how you completed the W-4 that you submitted to your employer. Change your allowances on the W-4 and you can either get more money back or owe more money to the IRS when it comes to filing time.

To re-iterate, the example above is very basic. In reality, the fast pass for filing taxes would only apply for those with W-2 income and not much else. It is not geared towards anyone with even a moderate level of complexity in their taxes since it does allow for additional factors which require additional calculations including:

- capital gains tax

- qualified dividends

- passive loss limitations

- business income and deductions

- tax credits (child tax credits, earned income credits)

- phase-outs

- alternative minimum tax

- etc., etc., etc.

While being able to do your tax return on a postcard is a noble concept, the IRS and government will have to clean up a lot of rules so that this can be available to more people. I fully support the idea of simplifying the tax code and making taxes more transparent. Now based on the example above, do you think your taxes could easily be filed on a single postcard or better yet an e-card? I know mine definitely does not qualify.

Also, if your taxes fit on a postcard today, I don't think you are maximizing all opportunities on your journey to Financial Independence. Sounds a bit harsh, but I'm coming to this realization myself.

File Your Taxes with H&R Block.