21 Financial Moves for 2021

“What the New Year brings to you will depend a great deal on what you bring to the New Year.” - Vern McLellan

Happy New Year!

2020 wasn’t exactly the year we all hope it would be. Many of us were pushed into situations that we didn’t desire, but the great thing about humans is that we are all very resilient beings. While a date and a year change shouldn’t stop us from making changes, it does give us permission to make the changes that we’ve long wanted to make, but never did because of fear: fear of failure, fear of success, fear of alienation and fear of the unknown.

This list focuses specifically on the financial moves you should make for a more successful 2021. Personal finances was a big topic in 2020. While the large and complex economic system needs a redesign, many of us individuals can do something today to change our own financial future and by doing so, we create our own personal financial security. With our own finances intact, we can be better equipped to change the system and help others along the way.

We encourage you to pick one or two of these financial moves to focus on the first quarter, then another two for the next quarter. Do not overwhelm yourself by doing too much.

This post contains affiliate links. See Disclosures for details.

#1 Write Down Your Money Goals

There’s power in the pen. Believe it or not, writing your money goals can be a huge step in ensuring you follow through on your goals. All dreams begin with an idea. The book Think and Grow Rich by Napoleon Hill is a motivational and actionable book to add to your reading list.

“Set your mind on a definite goal and observe how quickly the world stands aside to let you pass.”

Writing down your money goals help keep YOU and YOUR MONEY focus. It’s so easy to get distracted by every shiny thing out there and if you don’t have overarching goals for yourself and your hard earned money, it’s easy to spend it on things and people that don’t add value to you life.

This is one of the reasons why we designed The Money Journal the way we did. It’s the flagship product of Sisters for FI and it is part money book, part journal, part accountability partner. Of course, you don’t need The Money Journal to start on your goals, a simple pen and paper will do.

2) Invest in Yourself

Many of us spend thousands of dollars for a college education. After college, we rarely think about continuing our education. Before 2021 is up, commit to investing in yourself. Figure out what skill, course or language will take your career or your personal life to a new level. 2020 taught us that we can teach and learn anything and everything online.

I know it’s easy to zone out in front of Netflix or Disney+, but if you really want something you’ve never had, you’ll have to do something you’ve never done.

A class, a book, a coaching session might teach you more and might be worth more to you in the end.

Here are some places to get started:

CreativeLive has some great classes to choose from if you want to improve your creative skills as well as how to manage our money as an artist or creative.

YouTube is free and has tons of great content. Not sure where to start, check out our curated playlists of money-related content.

Your local library can be a great source of books and workshops. Find a list of recommended financial books here.

To ensure you spend money wisely on furthering your knowledge, create a line item in your budget so that you allocate funds towards a class. Doing this makes it more real and concrete.

#3 Get Life Insurance

Sadly, we learned in 2020 that many people did not have the funds to take care of themselves upon their death which put many families in a financial predicament. GoFundMe became prevalent as the means to help families survive financially. For 2021, we encourage you to protect your loved ones by investing in yourself and in your loved ones. Life insurance is less about you, but more about the people you leave behind. If your partner, children or other dependents depend on you for survival (through income OR caretaking), life insurance is highly critical. Get it an at early age when you are younger and healthier. Your premiums will be much lower and it offers you the benefit of great peace of mind.

If it’s just you and no one depends on your income, then life insurance may not be necessary just yet, but also keep life insurance as an option not only in the event of your death, but also in the event of a disability. Better to protect your family for a few dollars a month than jeopardize their well-being.

The amount of life insurance will vary depending on your needs, but a little is better than not at all.

#4 Get Out of Debt Quickly

Debt is not the only way.

With debt, each day that you wake up, you are working against the clock. You must earn enough money to cover today’s living expenses, plus yesterday’s expenses and interest. Debt free is possible! Work towards paying down debt as quickly as possible. You are not tied down to a monthly payment. Relish the joy of feeling #paymentfree. Whichever method you choose to pay off debt, be it high interest rate first or lowest amount, get diligent about paying it all off. The faster you can pay off debt, the faster you can invest and make your money work for you.

Our favorite debt free tool is free is by Vertex42. It’s a simple spreadsheet for Excel and Google Sheets that allow you to track all of your debt and figure out the best way to tackle them. You got this!

#5 Negotiate Your Bills

You’d be surprised at what a few minutes with a customer rep can net you. Review your bills and tackle those where you’ve been a long-time customer. Use this as leverage to get a discount on services that you’ve been using like phone services, cable, gym, etc. Americans fear negotiation because we aren’t taught how to do it. The best way to negotiate is to come prepared with information. Remember that No should be the start of a negotiation. Take a look at this book to boost your negotiation confidence.

Know how long you've been a customer

Know the company’s current promotions

Know their competitor rates (shop around)

Know what you want and are willing to bargain for

It costs more for a company to get a new customer than to retain one so take advantage of this and work to negotiate lowers rates for services you use often.

#6 Sell Your Clutter

2020 was the year we spent a lot of time at home. Perhaps, this is when you realized that you didn’t have enough space, but was it a space problem or a stuff problem? Let 2021 be the year you live a less cluttered life. Look around! All of that stuff around you was once money. All of that money was once time. Could you have paid off debt already or traveled somewhere amazing instead of buying all of that stuff? How much time have you missed with loved ones because you had to go exchange your time for money (work)?

There are many ways to declutter and organize. One method is by Marie Kondo. One of Marie’s first ask of her clients is to place ALL of their clothes on to their beds (not on the floor). Undoubtedly for everyone that does this, the pile is very high. Stuff equals Money. How much of your time and energy were used to buy, maintain and store those clothes? We rarely think about the external costs of a purchase, but it adds up. Having an extra room to store items means heating extra square footage or paying rent for closet space. Having multiples of items means we spend more time looking for things than actually enjoying the object.

Cutting the clutter can help you reclaim money and time. Don’t neglect it as a power move for 2021.

7) Increase Your Retirement Contributions

A basic move and one that you will find in every and any list concerning personal finances. So why aren’t you contributing yet? What’s stopping you? If your company matches contributions, it’s the easiest way to double your money. Where else can you get that kind of return? Plus, if you also think about it, a company match is technically part of your compensation so why not take advantage of it. If you don’t, you are literally leaving money on the table.

If you are not contributing, contribute at least to the company match.

If you are already contributing to the company match, increase your contribution by 1% or 2%.

If you received a raised, increase your contribution the same amount as your raise. This helps reduce lifestyle inflation.

For 2021, the IRS contribution limit is $19,000, add to that the company match and you could be walking away with a significant nest egg. Don’t forget too that contributing pre-tax lowers your taxable income for the year. Check your first paystub at the beginning of the year and adjust your contributions. Part of your increase in contributions will be offset by a a decrease in taxable income. Retirement may seem far for many of us, so don’t think about retirement at 65, think about financial independence earlier on.

#8 Contribute to your HSA or FSA

I don’t remember the HSA and the FSA being advertised heavily when I was in corporate so I want to tell you to review your health plans carefully. An HSA is a Health Spending Account and an FSA is Flexible Spending Account that allows you to set aside money for health expenses like deductibles, and other medical and dental costs.

Why contribute? It’s essentially forced savings for future medical costs, which increases as we all get older. An HSA normally is tied with a high deductible health plan and any unused balanced rollover into the next year so any unused money can accumulate over time providing you a great cushion for potential medical emergencies. The HSA has a triple tax-advantage in that the money you put isn’t taxed, the money grows tax-free and the money withdrawn isn’t taxed as long as it use used for qualified medical expenses. Many of us have the advantage of being healthier in our youth so getting a higher deductible and using an HSA can be positive move for your future self. Saving early in your career can provide you a nice sum later on to use for maternity costs, children’s medical costs, and other healthcare costs as you get older.

An FSA is “use it or lose it” so you’ll have to plan your expenses accordingly. The FSA must be used up by a certain date or you risk forfeiting the money. The FSA now also covers over-the-counter medications and feminine products finally. If you do have an FSA with funds, don’t forget you have to use it up by the deadline set by your employer which can be Dec 31 or March 31 of the next year. Head to HSAStore.com or FSAStore.com and see what’s eligible.

Personally, I used HSA and FSA to cover the costs of my LASIK surgery a few years ago and a dental procedure that was more than I expected.

#9 Get Involved

One of the big things that has come to light in 2020 is how a lot of the laws that are in place that deal with our money are set by elected officials. Those federal #studentloans you've been diligently paying off, those rates are set by Congress. That 401K you've been contributing to, that was due to Congress passing the Revenue Act of 1978, which included a provision that was added to the Internal Revenue Code — Section 401(k). Those local taxes you pay for, the budget and allocations are determined by your local officials. The national minimum wage was created by Congress under the Fair Labor Standards Act (FLSA) in 1938 and continues to be amended. Some states and local governments continue to set minimum wage levels higher than the federal level because the people spoke up.

⠀

Make sure your vote counts. Figure out where your rep stands for issues that are important to you by going to their website and calling their office. The staffers can help you obtain information.⠀

#10 Read Your Employee Benefits Handbook

How many of us really read the Employee Benefits Handbook? There’s most likely a treasure trove of other benefits that you could be missing out. A common one is the Employee Assistance Plan that can get you access to counselors for a wide variety of needs including financial advice. It doesn’t hurt to ask if your company covers help in dealing with a personal issue. If you and your partner both get benefits, review those plans and handbooks to see which fits your needs. Accessing some of these benefits can greatly reduce any financial burden you may incur.

Due to the pandemic, many companies have also modified their benefits as a sign of the times so it’s important to check what’s change. Many people under estimate how much more value they can get out of their jobs by signing up and enrolling for certain benefits.

Learn more about common employee benefits and why and how you should take advantage of them.

#11 Check Your Investment Allocations and Fees

January is a good time for an investment checkup especially after the year we’ve had. The stock market was hovering over record highs in 2020 which means your portfolio may now skew towards certain sectors or stocks . Re-balance your portfolios as needed. What does this entail? It means selling stock or funds so that your ratio of stocks vs. bonds. vs. cash is as you desire. Normally, over time, as the economy shifts and your goals changes, your allocation should also shift We personally like Personal Capital (review here) for aggregating multiple accounts in one place. This is especially helpful if you’ve got old 401Ks, IRAs, investments, etc. in multiple places. Their free tools provide a way to see what kind of investments you are holding the most and the fees associated with them. Fees add up and eat into your returns so choose funds that have low expense ratios so you keep more of your money. Getting that holistic view can help you spot over-allocation, duplicates and unused cash reserves.

#12 Start Your Side Hustle

Progress over perfection!

If are looking to earn money on the side, start your side hustle today. Your side hustle doesn’t have to be perfect. It doesn’t have to have the perfect name, logo or tag line. If you can provide a service that others value and will pay for, then do it. As you hone your skills over time, your craft will get better, as you work with more clients, you’ll understand their needs better and then you’ll be better equip to formulate a plan for moving your side hustle to a full fledged business.

We’ve not utilized yet the true power of the internet and more specifically the power of e-commerce and online learning. 2020 showed us that businesses need to pivot quickly to the changing needs of customers. In the same way that you’ve had to change your shopping, dining and consumption habits, your side hustle and the solutions you come up with should pivot to solve the new needs of the new normal.

#13 Set Yourself for A Raise This Year

If your company hasn’t completed performance reviews yet for 2020, it’s time to remind your boss how great of an employee you are. This can be as simple as sharing some of the great projects you’ve completed from the year. What many employees don’t realize is that your manager should be armed with data so that they can hype you up behind closed doors. When managers make decisions about bonuses and increases, they’ll be looking at their own records of your work, but many managers are so busy that this may be difficult for them to do, couple with the fact that like you, your manager probably also had to juggle working from home, kids, and other responsibilities so remind them how good of an employee you are (even if 2020 was a mediocre year).

Then, when that raise hits your bank account set it up so that you don’t see it. Pay your future self first. Remember that at some point, your future self will stop working. Who will pay you? If you think ahead, you can set yourself up to pay yourself. By “ignoring” your raise, you won’t be tempted to spend it.

Lifestyle Inflation is a very real phenomenon in which our expenses increases as our income increases. Most of it due to the idea that “we deserve” new and better things because we’ve worked so hard for it. That may certainly be true so we all need to find that balance between treating our present selves, but also ensuring our future selves are cared for.

Before that raise hits, increase your retirement allocation or saving allocation by a similar percentage or increase your automatic deduction to a debt payment. The goal is to keep you living at the same rate as before and socking away that money so that you can buy yourself time later on.

#14 Review Your Credit Report

A lot happened in 2020 so it’s prudent to review our credit report to ensure everything is what you were expecting to be. If you have future plans for large purchases post-pandemic, now is the time to ensure your credit is as good as you can get it. Your credit history and score is a large factor that determines how much gets lent to you and what interest rate. It’s important to check your credit report at least once a year. There’s Federal Law that mandates individuals be able to check their credit report for free at least once a year. You can head to https://www.annualcreditreport.com to do so. It will allow you to pull up reports from the 3 credit bureaus. Check it for errors and correct errors right away. This is a good way to also check that payments are being reported properly and that no new accounts were opened without permission. Lenders heavily rely on the credit report to rate you as a borrower so it’s important that you be diligent with what appears in this report.

#15 Remove Saved Credit Card Info from Your Browsers

If you found yourself purchasing blogger recommended items on TikTok, Instagram and everywhere else on the internet, it’s time we hit Pause on that. One way to do that is to make it inconvenient for you to purchase items online by removing saved credit card info from your browsers or certain shopping portals. Of course, if the desire to purchase is strong, you can readily pull out your wallet, but sometimes adding a small, but effective barrier of having to grab your wallet can result in less spending.

This little hack has it’s influence from the red velvet rope that clubs have outside the door. This simple idea actually deters people from just going up to the door and going in.

#16 Save for the Things that Are Likely to Happen

Statistically, many of us will follow the same path as we age and grow older. We will all want shelter, people to love, time and money to do things we like, and all of us will eventually stop working (because our bodies no longer allow us to or because we don’t want to.) It’s good to start planning for these things now.

Sorry to say that Prince Charming won’t be coming to rescue any of us. The odds of winning the lottery is pretty low. Our parents have yet to live their retirement so the odds of us getting an inheritance will be low. Lastly, the world will not end tomorrow despite what all the news channels reported in 2020.

We are all bad predictors of the future so don’t try to predict it. Hi and Bye Corona. Instead look at the statistics of the likelihood of marriage for young adults, 100% retirement for all of us, your wants at having children, your needs for having a place to live, etc. Save for those, because as much as we would like to think that we are all unique, most of our needs are the same so save for that house, for that wedding, for your future children, for retirement regardless of how far they are into the future.

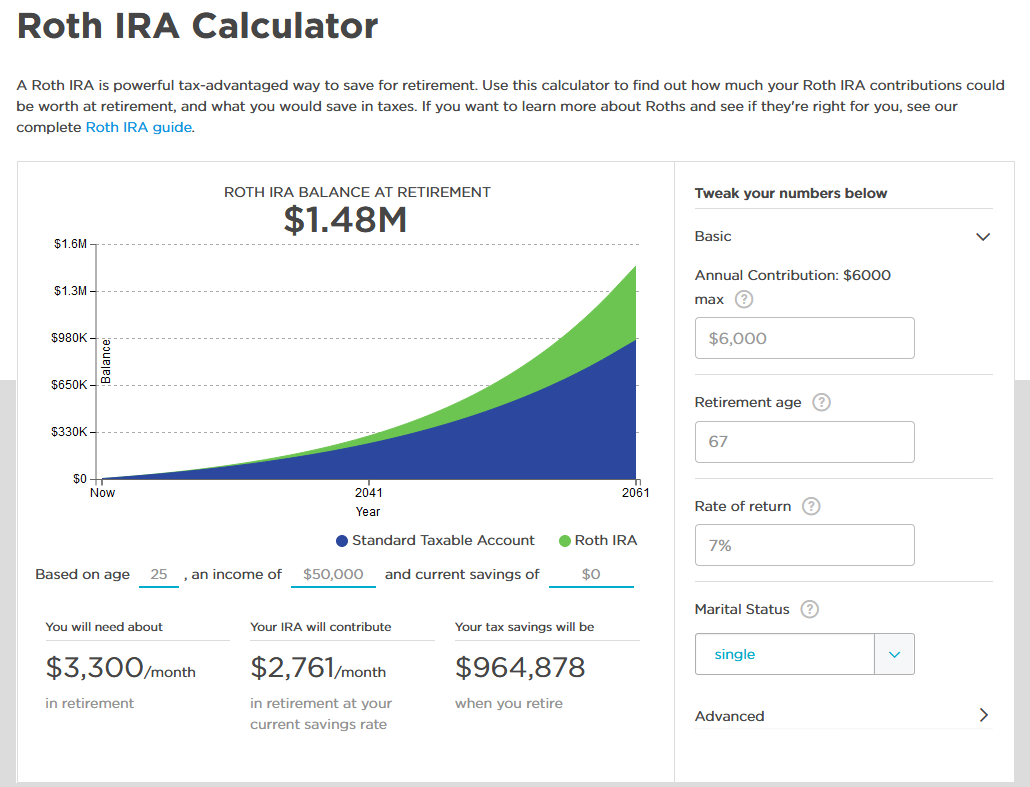

#17 Contribute to a ROTH IRA

The ROTH IRA was born in 1998. It’s practically a Young Millennial and what that means if you are a Young Millennial or a Gen Z is that you have the opportunity to save for your future today. A ROTH IRA is a great savings vehicle because you pay taxes today and your money grows tax-free and can be withdrawn without penalty when you are 59 1/2. There are exceptions to this rule that you can read more about over at irs.gov. The best part about a ROTH IRA is that it is not tied to any employer. As long as you have earned income you can open and contribute to an IRA up a maximum $6000 for 2021. There are income limits, but don’t worry about that for now. The IRA, which stands for an Individual Retirement Account, has slightly of a misnomer because it’s not just for retirement. The funds can be used for education and home buying as long as you meet certain requirements. I’ve used a part of my IRA as down payment for a condo.

If you contribute $6000 a year towards a ROTH IRA (income limits apply) starting from age 25-65 and have a conservative rate of return of 7%, you’d have a hefty nest egg of about $1.4M. Not too shabby right. Here’s a simple calculation that you can do over on nerdwallet.com.

Sample ROTH IRA Calculation.

Consider opening an IRA this year and automatically it fund it a few dollars a month. As you get used to money being taken out, increase it. Again, it’s another source of savings. A reminder that a ROTH IRA i sjust a savings vehicle so you’ll need to select what to invest in.

#18 Schedule Those Money Dates

We always have the best intentions when the new year starts so before life gets hectic, schedule those money dates today. Make it a personal commandment to meet with yourself, with your spouse and with children or parents (if needed) to have a conversation about money. The goal is to inform and get feedback as to the state of the family’s finances. This will require that you and others be honest and upfront about money worries. Money is always a touchy subject but push forward. It’s important that you, your spouse and other family members are aware of your financial situation in case something happens to you.

To make money dates successful, schedule it on everyone’s calendars ahead of time. Crowd source an agenda so that everyone’s needs are addressed. Make sure there are no distractions. Come with with open mind and listen to each other. Come up with a list of action items for everyone to do moving forward.

If you need help talking money with children, check out this resource.

If you need help talking money with your aging parents, here’s an article to help.

If you need ideas on how to get your finances in order while kids aren’t in the picture yet, read this article.

#19 Plan Your Giving

A great part about having money leftover after spending, saving and investing is that you have the opportunity to use it for good. Money is just a tool so consider who you can share it with. Perhaps, it’s not money that you’ll have more of next year, but time, who can you help in the Year 2021? Write down a list of people and organizations that you want to help. Start with those around you, local organizations because when we lift the community around us, it benefits us all.

#20 Rest and Recharge

More than anything, I think 2020 taught us to slow down a bit, rest and recharge. If you are fully pursuing FIRE, I encourage you to re-think what the RE means. It may be using the power of your savings to REST and RECHARGE while you are young. Hustle culture is real and alive and it’s a great way to earn more income, get out of debt faster, etc, but as with all things, we all need balance. Your greatest asset is you and your health. If you work yourself to the bone, you won’t be able to contribute as much to your future self, your family and your community. Find a balance that works for you when it comes to pursuing your goals that doesn’t jeopardize your well-being. After all, health is wealth!

#21 Join a Money Group

We absolutely need to normalize conversations about money. For the new year, commit to joining a money group be it online via Facebook Groups or in-person. Find space where you can openly talk about your money concerns without judgement or fear. Hear and listen to what others have experienced when it comes to money. Sometimes, we don’t have to make the same mistakes. I consider myself an #eldermillennial so I am happy to share my money mistakes. Many people have walked the same paths as you and can offer your advice and tips on making money work for you. Don’t be afraid to ask.

If you can’t find a group that you click with, form one. Get your friends together and setup your own tribe.

Sisters for FI has it’s own Facebook Group if you want to join. You don’t have to it alone.

Bonus Tip

Move your money to institutions that are doing more good. One of the concepts we’ve talked about here is the pursuit of financial independence in a socially conscious way. How can we use our money for good? Is life really about profits? What about people and planet? For 2021, consider putting it in your list to move your money towards companies that are investing back into local communities or investing in alternative energies or in companies making changes to be more equitable. Our values matter and we all need to be thinking about how our money can used to make a better world, not only for ourselves but for the future and the people around us.

Did we miss any? What’s your #1 financial move for 2021? Let us know in the comments

Sisters for Financial Independence: 21 Financial Moves for 2021